Bird's that can't Fly

Issue 12 (05/01/2024): The rapid rise and fall of micro-mobility startup Bird reflects larger uncertainties around the e-scooter industry's future and it all comes down to unit economics

Having lived in a college town for the past three years means for cold walks to large lecture halls, being happy with 40% on a computer science midterm, and near misses with the millions of scooters that zip past you daily. It’s as if there are more scooters than students on campus and that’s not just a phenomenon I saw at Cal, but almost every campus I had been to in recent years. Personal E-scooters have become a staple much like a HydroFlask or iPad in the new wave of what’s cool and seemingly useful to be a successful college student.

Simultaneously, however, we have seen the rise (and impending fall) of various micro mobility means, we saw one of the quickest stories of being founded, SPAC, delisted, and now bankruptcy for a company that once was valued at $2.85 Billion. Is Bird a microcosm of what’s yet to come for the micro mobility industry or just an inopportune perfect storm to an unfortunate company. Bird at one point operated across 200 cities in 3 continents and now is filing chapter 11 in its seemingly most active country: The United States.

0-1 Beginnings of Bird

It ain’t pretty. Overnight like an infestation, Santa Monica saw piles of scooters wreathed across the pavements in September 2017 with onlookers confused on what to do with them. Some upright and properly kept, whilst others laid across the ground looking half broken - kind of a foreshadow of what’s to come. But the move was bold and that’s what investors saw. The shock and awe tactic set the stage for early VC funding and a future valuation exceeding $2 Billion.

Business Model

Bird relies on an “asset-light business model” using fleet manager programs to oversee operations. Essentially, contractors can lease fleets of scooters and it’s up to them to deploy these across a city. Let’s walk through an exercise to understand the unit economics of what makes a scooter profitable for a company. This exercise will develop a conservative and an optimistic view of the metrics but also identify the levers that were required for e-scooter operators to be successful, and maybe showcase on why it fell short.

A lot of inspiration for the model and the initial assumptions was taken from Haje Kamps and Alison Griswold, with updated numbers as Bird has changed its pricing structure and the costs of goods have ebbed and flowed in recent years (Thank you Haje Kamps!) . Bird uses the Xaomi Mi Electric Scooters which can be found at $425.00, however, with the bulk that Bird expects, we can take $100 off the top (the assumption is taken from similar percentages taken off of bulk after reading various public 10Ks and pitch decks from mobility companies). Once the tracking, labor, and shipping are accounted for, the total cost per unit is $455.00 (Refer to Figure 1)

Figure 1: Acquisition cost of Purchasing the Scooter and Adapting it for Bird

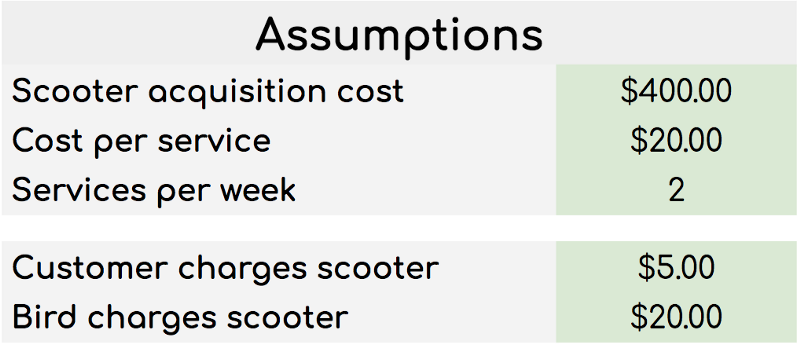

Figure 2: Assumptions taken from Haje Kamps

Regarding the assumptions, I’ve taken the assumptions made by Haje Kamps (Figure 2) the charging costs on Bird depending on if Bird charges it or a customer, with a 50/50 split. Of course, the Scooter cost and the servicing costs are different with the new information that is more current so they have been altered (Refer to Figure 3).

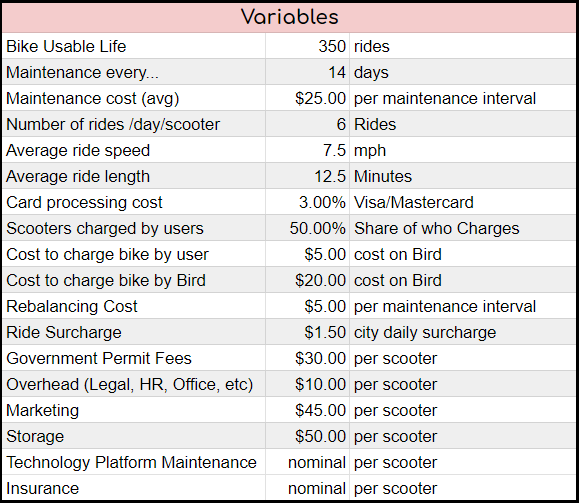

Figure 3: Variables for both Revenue and Cost Factors for E-Scooter Usage

Figure 3 highlights a long list of assumptions made that will impact the costs and revenues in the unit economics. Not to bore anyone with this list, however, for the nitpicky, the list has been provided. Fast facts here include the following:

Scooter Usable Life: 350 rides

Maintenance occurs every 14 days at $25 per interval

Average Ride Length is 12.5 minutes

Number of Rides per scooter per day: 6 rides

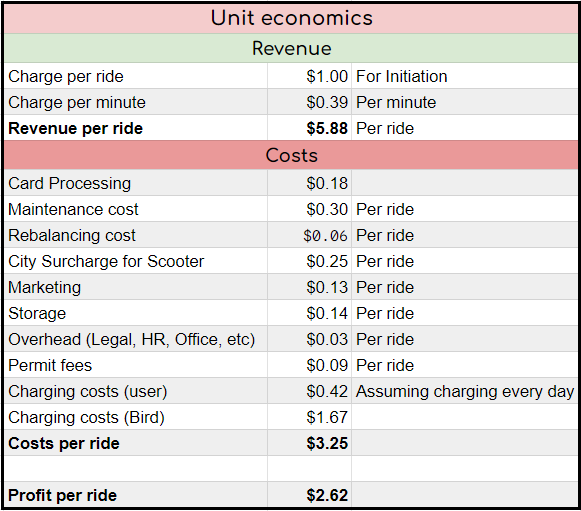

Figure 4: Unit Economics of Scooter Usage to Establish cost and profit per ride

Bird would charge $1.00 for initiating a ride and $0.39 for every minute riding thereafter (used to be $0.15 in the good old days). Fast forward all the nitpicky calculations, and we get the following conclusions:

Revenue per ride: $5.88

Costs per ride: $3.25

Profit per ride: $2.62

This leads to a gross margin of 23%, which, for a lack of better words sounds rather appalling. The gross margins sounded far better when Bird was pitching to VCs to raise over $880 million over 12 rounds with the latest being $100 million in May of 2022 (venture debt funding after SPAC). Of course, the margins I found are with many assumptions that may be completely misguided, but still provides a flavour for what the numbers may look like with an outside-in approach. For the sake of curiosity, Below are 2 appendices with 2 different assumptions regarding the lifetime rides as well as the number of rides daily to suggest how that affects gross margins (TLDR: it doesn’t look that much more optimistic). However, with the current assumptions above, it will take 170 rides to break even, which amounts to about 28 days with current assumptions.

Short Lifespan: Start, SPAC, Suspended, Sunk

Usually it takes a company about 9 years to go public, Bird started, went public, was delisted, and bankrupt in 80% of the time. Here’s an homage to chart what really happened. In early 2021, Bird, after a dozen rounds of funding, decided to venture for a SPAC-led audition to go public with the intention to aim for profitability by 2023 (as reported by Techcrunch).

SPACs are cool. But they are more trendy than useful. For those of you who don’t know what SPACs are, they are known as “Special Purpose Acquisition Companies”. Traditionally, a SPAC is when a company with no commercial operation is formed and set to raise capital for the purpose of acquiring or merging with an existing company.

In November, Bird merged with Switchback II via SPAC to list in the NYSE at a valuation of about $2.3 billion under the ticker BRDS (Allbirds beat Bird to the BIRD ticker). The share price tumbled, enough to receive a formal warning from the NYSE that they were trading at a price that was too low. NYSE delisted Bird and it began trading on the OTC Exchange late September 2023. Three months later, it filed for bankruptcy in North America.

Micro Mobility Mayhem

Back the unit economics and how that impacts the micro mobility industry. The Micro Mobility Global Market Report states that the expected Growth Rate and Market Size through 2027 is set to be 18.2% and $102.14 billion respectively with the largest growth being public transportation and the Asia-Pacific region. The growth rate for scooters as a mobility option is only but a fraction of these staggering numbers. Covid-19 put an optimistic veil on Bird and the industry coupled with VCs being far more optimistic about startups, it seemed like the perfect storm. Sadly, all storms one day come to an end.

Propitious Pandemic Prodigy?

We all talk about how the pandemic catalyzed venture funding for the 24 months from the start of the pandemic. Given that Bird already had raised their Series D and over $500 million prior to February 2020, they were the perfect company to go into the 24 months where VCs wrote blank checks. Unfortunately, however, this speedrail train derailed at the first sight of going public. They were valued at $2.85 billion, however went public at $2.3 billion and raised post-IPO debt at even lower valuations.

It all comes down to the unit economics and poor margins. In 2019, the then CEO, Travis VanderZanden stated, even after it had seen a revenue decrease of over $15 million, that Bird made $1.27 on every ride on its Bird Zero scooters which accounts for 75% of the fleet. However, this was back when they were charging 15 cents per minute, not 39 cents. Using similar assumptions to 2019, with the amended 39 cents and similar number of average daily rides, Bird makes $2.62 per ride, however, paying 39 cents per minute does not sound as enticing anymore. Furthermore, the $1.27 a ride was marked during the summer when you see flocks of interns rummaging through cities to use technology like this - which once again - skews the numbers to make Bird look optimistic.

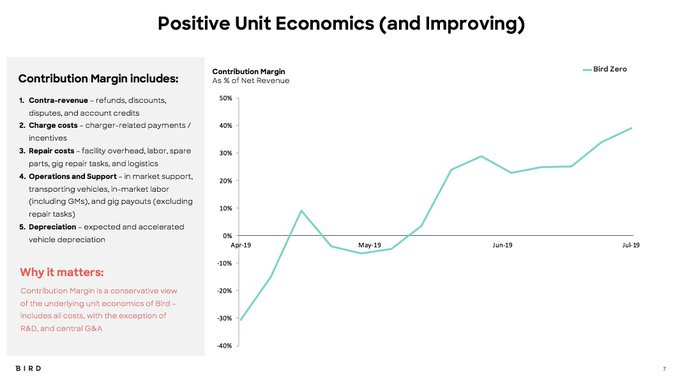

But the emphasis needs to not be put on how much each ride makes, but more to the margin. That’s what VCs care about, and that’s what you should care about too. Figure 5 shows the visual that Travis VanderZanden provided as backup for his tweet and the contribution margin looks bleak, but it is improving, I guess?

Figure 5: Travis VanderZanden posting the Unit Economics of Bird from April 2019 to July 2019

Cities are cracking down and administering city taxes, surges, and permit requirements. Furthermore, these scooters are not built for the timid, cold, and frankly, heartless streets of cities that they operate in. Costs are increasing and it’s hard to believe customers still using E-Scooters if the price per minute exceeded anything beyond $0.45. This arguably may be the first pillar to fall to arrive at their impending Chapter 11 filing - the gross margin being at 23% according to the “back of the napkin” calculations in Figures 1-3 as Haje puts it so eloquently in his article.

Future of micro mobility

It seems too late for Bird to spread its wings, but could the phoenix rise from its ashes or perhaps breathe some new life into competitors trying to achieve the same thing?

For a business that relies so heavily on utility and the costs, and by extension, the bottom line it all goes back to unit economics. So to really understand the future of e-scooters, let’s understand the levers that companies need to push their numbers higher in. It comes down to increasing revenue by either increasing the lifetime rides per scooter, or increasing the number of rides per day and by decreasing the costs which can be achieved by rethinking charging costs, maintenance costs, or just buying cheaper (yet robust) scooters.

Levers for e-Scooters

Scooter Design and Hardware

The most basic optimization falls down to designing more robust, durable, and modular scooters. The three intentions with this would be to increase the number of rides that a scooter is able to do in a lifetime, reduce the frequency of maintenance, and administer modular batteries to reduce the charging costs. Sturdier builds may be required as well to vandal-proof and increase the lifespan. Modular to improve repairability and improve battery range and reduce battery maintenance costs may be a good idea too. This would increase the MSRP of the e-scooters, but ideally reduce all the other costs and increase the lifetime to bolster up the margins.

Daily Ridership

Ridership on scooters are most probable during peak hours which occur in tandem to office/school timings. The only issue is that two people can’t exactly use the same scooter to get to work at 8:30 am. Therefore, ridership has always stayed low during any hours apart from work. Offering price reductions or marketing usage outside these hours may increase the daily ridership from the average 6 per scooter per day. The appendix highlights how increasing this number will affect the margins (it’s not excellent, but still a step in the right direction).

Price Optimization

Everyone hates price surges and perhaps for a product that isn’t exactly sticky, price surges may not be the best way forward. However, if a scooter could employ geography based dynamic pricing, instead of time based dynamic pricing, there could be a benefit.

Imagine you are off to work, you drop it off right below your 65 floor building. For the next rider, there could be a price surge as you are taking it from a higher foot traffic area. As long as this doesn’t reduce the number of rides each scooter does on a daily basis, it could account for more income.

Additional Optimization Methods

Regulatory Collaboration

Many city dwellers find scooters scattered on pavements rather off-putting and it has reflected in regulations. Companies have been hit with regulatory taxes and surcharges and it seems like they are here to stay. It would be worth aiming to have regulatory collaborations

Rebalancing, Demand Prediction and Predictive Maintenance

Scooter rebalancing continues to be a growing cost for fleet owners. Fleet owners could utilize demand prediction tools to optimize their rebalancing efforts during the late hours of the night. Of course, with the addition of lighter, modular, and in-built predictive maintenance scooters, the costs of rebalancing and maintenance would already fall. Predictive maintenance sensors could dictate if a scooter required maintenance earlier, but also encourage scooters to not be checked for maintenance should they not require it.

Dedicated Infrastructure

These scooters are being vandalized more often than not and being parked in inconvenient locations. Dedicated parking locations may reduce such issues and potentially increase the lifetime of each scooter. Perhaps even doing what Citibikes has achieved with dedicated lock zones may be a phenomenal idea - but certainly will increase infrastructure and overhead costs.

Concluding Remarks

It’s too late for Bird and the impending demise of such companies seems probable with such harsh margins. For a company like Bird to succeed, they really need to focus on increasing the lifetime of a scooter, getting daily ridership up, and decreasing costs of maintenance with modular batteries. But doing all of that costs money, and conjuring up ways to increase daily ridership has proven a very challenging task.

But what I believe most is that such products are not even useful in terms of costs. Say you take two rides a day to and from work, and go to work 300 days of the year. That means you are spending about $5.88 per ride (if it’s a 12.5 minute ride), which is already above $3500 per annum. Just buy a scooter at that point. Needless to say, these scooters are useful for infrequent and impromptu rides. But even if you ride twice a week, that’s still $611.52 a year. Again, just buy a scooter.

Of course hindsight is 20/20 and Bird’s chapter 11 demonstrates the complicated and gloomy unit economics of rental scooters. But this just puts a microscope on Bird’s competitors and puts a yellow light on VC investments on micro mobility. This is all for good reason.

I’ve never been an avid user of such scooters, both rental or personally purchased. But I know of many that have bought scooters and a few that use the rental ones - mostly infrequently. It’s a tough market to be in and I look forward to interesting solutions.

Appendix

Appendix 1: Scooter lifetime P/L with the assumption of 350 rides and 6 rides per day per scooter (Format inspired by Haje)

Appendix 2: Scooter lifetime P/L with the assumption of 500 rides and 8 rides per day per scooter (Format inspired by Haje)

Bibliography

https://techcrunch.com/2021/05/12/bird-rides-to-go-public-via-spac-at-an-implied-value-of-2-3b/

https://techcrunch.com/2021/11/02/shareholders-approve-bird-spac-merger-stock-promptly-falls/

https://qz.com/1325064/scooters-might-actually-have-good-unit-economics

https://blog.bolt.io/financial-levers/

https://techcrunch.com/2021/11/02/shareholders-approve-bird-spac-merger-stock-promptly-falls/

https://www.crunchbase.com/organization/bird/company_financials

https://app.dealroom.co/companies/bird

Image Credit: Bird (Found on TechCrunch)