As Cheap as Chips... Kinda

Issue 8 (17/08/2022) - An Article Looking at the CHIPS and Science signed on August 9th. Looking into what the act is about, what it's intentions and aims are and how does this affect the startups.

Now the title is a little misleading, and a little more posh than what my target viewers expect; however, it does hold a certain level of truth to it. Some of you may have heard of the new CHIPS and Science Act that was signed on August 9th by President Joe Biden. It’s full form is “Creating Helpful Incentives to Produce Semiconductors (CHIPS) and Science Act (props to the individual who came up with the title that lead to such an acronym - honestly very impressive).

This act has been signed to revitalize USA’s hold on the semiconductor market, that has been slowly outcompeted by the East Asian markets - and to develop a stronger relationship with these aforementioned markets too. It aims to seal the long term scars brought on by not only the pandemic, but decades of losing focus from the semiconductor race that once was a core priority for the States. To the nation, this should ideally translate to increasing domestic manufacturing, creating long term job growth and security, and seal the foundation for future industry expansions as semiconductors are practically used for anything and everything you can think of.

“Yash, why are you talking about a macroeconomic act in a blog titled Startupology”

You are correct, so very correct. Mainly, I’m writing about this because it is interesting and a very good friend I had the opportunity to work with over the summer recommended that I write about it. But I will highlight the significance of this within the startup ecosystem too… after I explain what even the CHIPS and Science Act even means. So, bear with me, or if you are solely interested in the effects this has on startups, small businesses, and future industry outlooks, skip to the How are Companies Reacting section of this article.

Party Like it’s 1949

USA, in the late 40s and 50s maintained the greatest market share in semiconductor manufacturing - seemingly excited from their new found discovery at the time. Fast forward to today, the nation captures a mere 12%, compared to 80% in the Asian markets. To exacerbate the idea further, USA produces none of the most advanced semiconductors: the ones that further technology the most, and bring in the greatest sources of revenue and are most in demand.

Fine Print

What does this act even mean? How is this Act really achieving all that it sent out to achieve:

The creation of a sector-specific interagency expert working group

Provides $52.7 billion for American semiconductor research, development, manufacturing, etc.

$39 billion in manufacturing incentives

$2 billion in legacy chip in automotive and defense industry

$13.2 billion in R&D

$0.5 billion in international information communications technology security and supply chain optimization

25% investment tax credit for capital expenses for manufacturing chips

The CHIPS and Science Act includes $1.5 billion for promoting and deploying wireless technologies

Authorized $10 billion to invest in regional innovation and technology hubs

Increased STEM opportunities in training, education, and recruitment

How are Companies Reacting

Of course, the semiconductor giants are incredibly excited. Within a week of its announcement, Micron, announced a $40 billion investment in memory chip manufacturing. These types of chips integrate into electronic devices such as computers and are set to generate 40,000 jobs in the construction and manufacturing sector. So 40 Billion sounds like a lot, but context is key to understanding the magnitude… Either way, statisticians expect the US market share in memory chip production should effectively rise 5x from 2% to 10% in the next decade with this hefty investment.

Given that it has been less than a week since the announcement, many companies are still deliberating over its long term benefits and how it changes the landscape. The main questions that arise from the CHIPS and Science act is where to move production. Is made in Asia still the go to game plan, or shall companies see a rise in the acts intended use and move to a Made in America model. The second question, perhaps slightly less important, is how the act skews towards Intel and Micron and chip manufacturers. How does this play into the hands of companies like Qualcomm and Nvidia, and where is the opportunity for startups to come in.

Made in America?

The Made in America movement is on the rise; however, can this Act spur growth of semiconductors back to the States? Companies with existing plants in Asia are left with a decision: Do we move? What are the sunk costs? What’s the long term upside and is it worth it in the end?

I don’t think the Act is resoundingly enticing enough to change existing plants overseas, however, may lead to satellite production centers for last mile delivery purposes into America - which nonetheless will still produce jobs, bring work to the States and have positive externalities.

I actively left out a lot of detail regarding how this will impact the macroeconomic landscape with regards to jobs, large tech companies, and things of that nature because I want to focus on the Act’s impacts on startups, small businesses, and founders. So after 800 words of context, here’s the exciting part of the article I’ve been looking forward to writing about all day.

Yash’s Long Term Thoughts

Personally

I love building computers. Back in 2017, I was convinced by a very close friend of mine to not purchase a Mac, but to rather build a PC from scratch. Best. Decision. Ever. I thought of upgrading my graphics card from a 1050 (it used to be a good card back in the day) to a far better one in 2022. However, chip shortages have made this resoundingly expensive for a college student with college rent and a need for overpriced coffee from Romeo’s Coffee. However, I doubt skyrocket prices of graphics cards, chips, and computer technology will come down significantly - this is more of a hope than a calculated assumption so please do not come after me if this isn’t the case. Hopefully, I get to see a day where my PC no longer has to settle for a 1050.

Is it really “As Cheap as Chips”?

$52 billion sounds like an absurd amount of money - which it definitely is - don't get me wrong. However, in the semiconductor industry, it isn’t as much as you might expect. A semiconductor plant has a rough price tag of $15-25+ billion dollars and by simple math that would mean enough money to build 2-3.5 ish plants. After deducting that, this investment seems a little less exciting; however, this initial push, with future injections from the private sector can see a domino effect coming along. It isn’t cheap, but the investment will definitely help start the growth, and especially enable startups to revitalize themselves after an unfortunate downturn.

Where Silicon Valley got its Name

The tale of Silicon Valley has many beginnings, but as its name suggests, semiconductors brought the area to life. The company Fairchild Semiconductor spun off from: Shockley Semiconductor Labs are the trendsetters of Silicon Valley. Shockley saw the “traitorous eight” leave the company to bring life to Fairchild Semiconductors. Fast forward a few years, these individuals were directly involved in starting Intel, AMD, Intersil, among other vestiges in the silicon chip industry.

My point in this short history lesson is that Silicon Valley attributes a long and rich history to semiconductors, and holds a soft spot for it. The industry that started off what we know and love may be the same injection to spur the markets.

Startup Trends and How the Chips Act is Fueling it

SaaS/XaaS

We all love SaaS, but what has set them apart most is the growth model. I envy any startup that is fortunate to either be a SaaS company, or be able to embody the “as-a-Service” model. This model that many startups are adopting enables agility and dynamism among startups at a fraction of the capital expenditure. This model is may bring rise to new Semiconductor startups, that appreciate the CHIPS act as initial funding, and utilize the XaaS model to fuel a recurring revenue model. Examples of this on grander scales include Dell, where “Dell Technologies on Demand” is a consumption based AaS service providing IT solutions that are customizable, agile, and affordable. Silicon as a Service (SiaaS) has seen a rapid rise in larger companies, something startups can look into to bring to the market in a cheap and niche manner. Chip usage, similar to how a taxi meter works, could be the core of this model, where customers are charged based on usage of these semiconductors and chip devices. This enables greater ability for customers to demand the speeds they require, without needing to alter hardware implementations regularly. This would be especially useful for AI companies who are providing chipsets in the cloud as well as IoT markets where silicon OEMs are bringing greater customer value.

Future Proofing Supply Chains

So the biggest problem most people will tell you regarding demand for chips, semiconductors or technology that requires them are the rising price tag in recent years and supply chain conundrums. With this act, money is flowing into the market and hopefully rectifying these supply chain problems. And, as aforementioned, semiconductors are relevant for every industry, especially in the tech bubble.

Autonomous Vehicles and Car Manufacturing

Original equipment manufacturers (OEMs) and startups such as Zook, Cruise, Pony.ai, among others, have invested over $106 billion in autonomous driving opportunities from 2010 onwards - especially in the advanced driver assistance systems (ADASs).

The demand for specialty automotive semiconductors has increased sharply, producible only in certain companies. The CHIPS act emphasizes high tech chip manufacturing which are required in autonomous vehicles (AVs). AVs require immediate responses and data processing capabilities as they respond to immediate and unexpected changes. These demand highly efficient and multiple interconnections between semiconductor chips and the vehicle - requiring very centralised electrical and electronic (E/E) architecture.

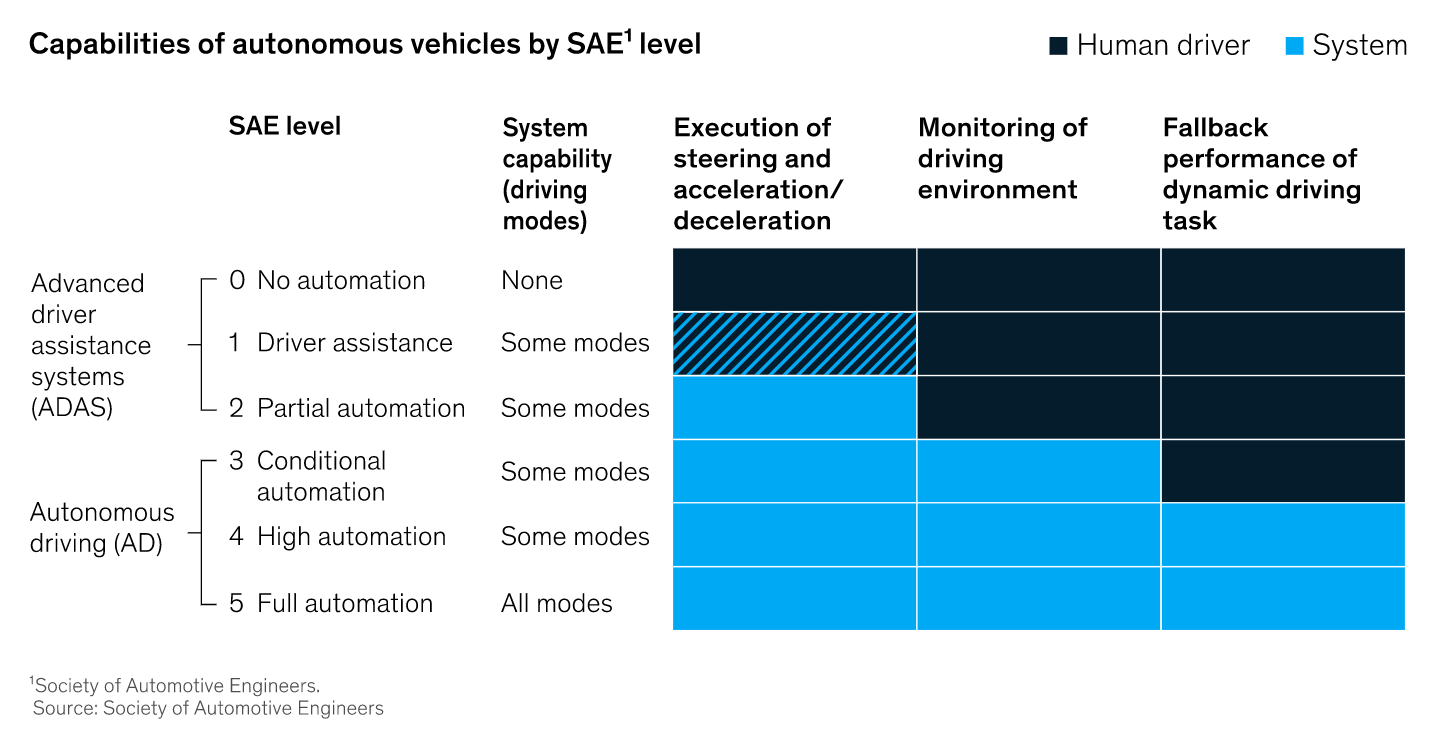

Figure 1 below highlights the scale of autonomous vehicles based on how little the driver needs to be attentive. It scales from SAE 0 level cars are your typical cars we know and love since 1885 to level 5 which implies complete automation.

This is important because cars between level 0-2 require standard chips. However, anything more advanced requires specialty silicon which are highly efficient, showcase rapid performance in data integration and assessing as well as are able to execute extremely complex software through high sensor inputs. Basically, what this convoluted sentence means is Level 3+ cars need special chips and Level 3+ cars are the cars that companies are most focusing on.

These chips are hard to obtain, expensive, and need specialised vendors that are not in the States. The CHIPS and Science Act aims to bring the manufacturing of said specialised chips back to the States, which is why the AV industry can increase its growth and development through better and healthier supply chain management and falling costs.

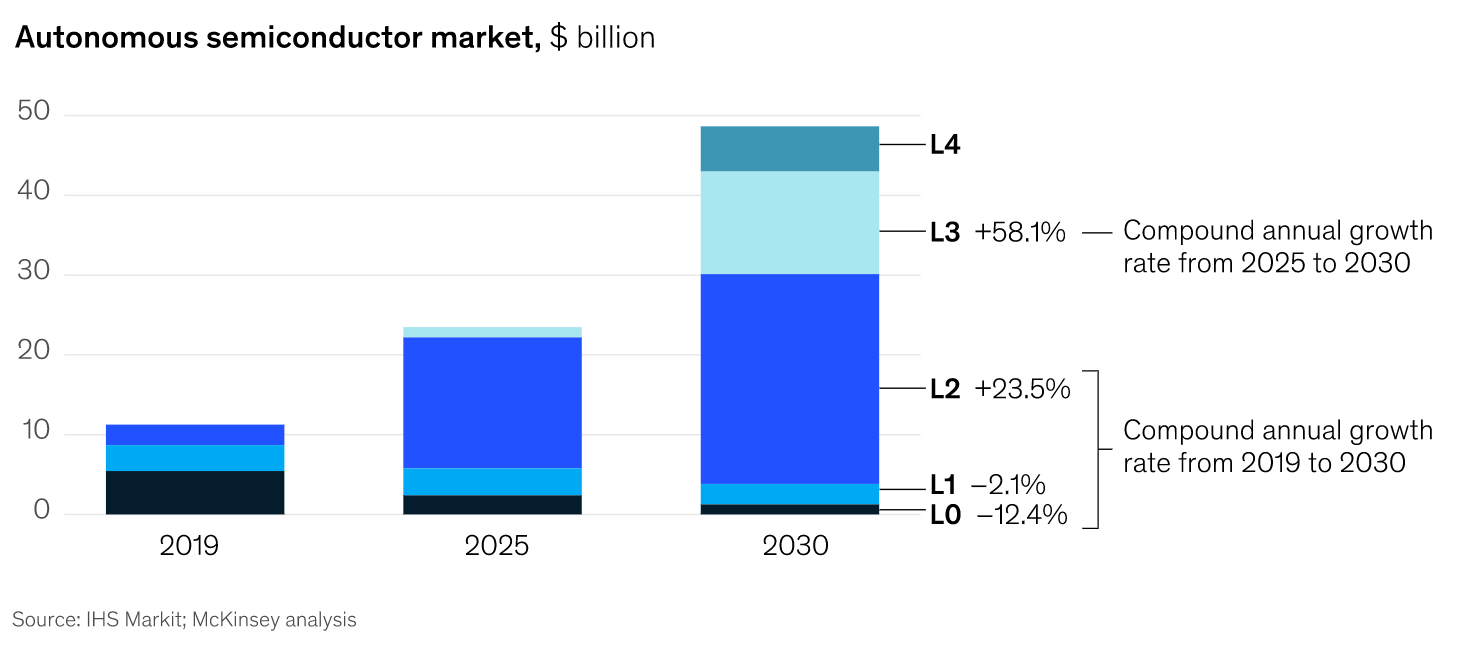

Figure 2 suggests the rapid rise in the semiconductor market for autonomous markets. This rise is synonymous with an increase in level 2+ cars. High-performance central-compute chips, such as domain control units (DCUs) and sensors, could see the fastest growth at 12%. Chips for decentral electronic control units (ECUs) and other sensors will grow at half the rate year over year from 2025 through to 2030 at 6%.

Startup Spinoffs

Chip design is evolving from general sentiment to specialised chips. Imagine a startup solely focusing on creating the most efficient chip to detect cars, road signs, and pedestrians. Niche market? Yes. Profitable given the trends we are seeing? DEFINITELY YES. The model for a single company could be to produce the most efficient chip specialising in such a submarket. Similarly, semiconductor manufacturing will develop its stake in various industries where the demand is soaring, be it defense, healthcare, or autonomous vehicles.

Revitalise Manufacturing Sectors

So this is a longshot, and I doubt the resounding affects will be lasting or at scale. However, I can’t help but understand that there will be some positive impact on the original intention of the CHIPS and Science act. Manufacturing may come back to US, to some degree. As producing chips will be cheaper than it was before in America, manufacturing will increase for products demanding these products.

Most probably, I expect rises in medical equipment, American cars, as well as to a certain degree TVs and smartphones to increase. But take all I say with a grain of salt as these are unsubstantiated claims, more educated guesses than anything.

Concluding Remarks

This article, by far seems to be a cacophony of stories, from silicon valley history lessons to a brief stint on OEMs and AVs with garnishing of macroeconomic sentiments and breakdowns of the Act. If anything, I hope this gives some clarity that large acts that are aimed at impacting large scale businesses and nationwide trends may have resounding, and perhaps, effects that were not initially expected or intentioned.

The most exciting segments remain in the AV space, where I hope this will supercharge the R&D of AVs, as well as enable greater innovation as it helps increase competition. From a startup point of view, the CHIPS and Science act should provide startups to spinoff into niche circles in the chip market, serving various industries.